Monetary Failure Is Becoming Inevitable

by Alasdair Macleod

ZeroHedge.comSun, 10/13/2019

This article posits that there is an unpleasant conjunction of events beginning to undermine government finances in advanced nations. They combine the arrival of a long-term trend of rising welfare commitments with an increasing certainty of a global-scale credit crisis, in turn the outcome of a combination of the peak of the credit cycle and increasing trade protectionism. We see the latter already undermining the global economy, catching both governments and investors unexpectedly.

Few observers seem aware that an economic and systemic crisis will occur at a time when government finances are already precarious. However, the consequences are unthinkable for the authorities, and for this reason it is certain such a downturn will lead to a substantial increase in monetary inflation. The scale of the problem needs to be grasped in order to assess how destructive it will be for government finances and ultimately state-issued currencies.

Introduction

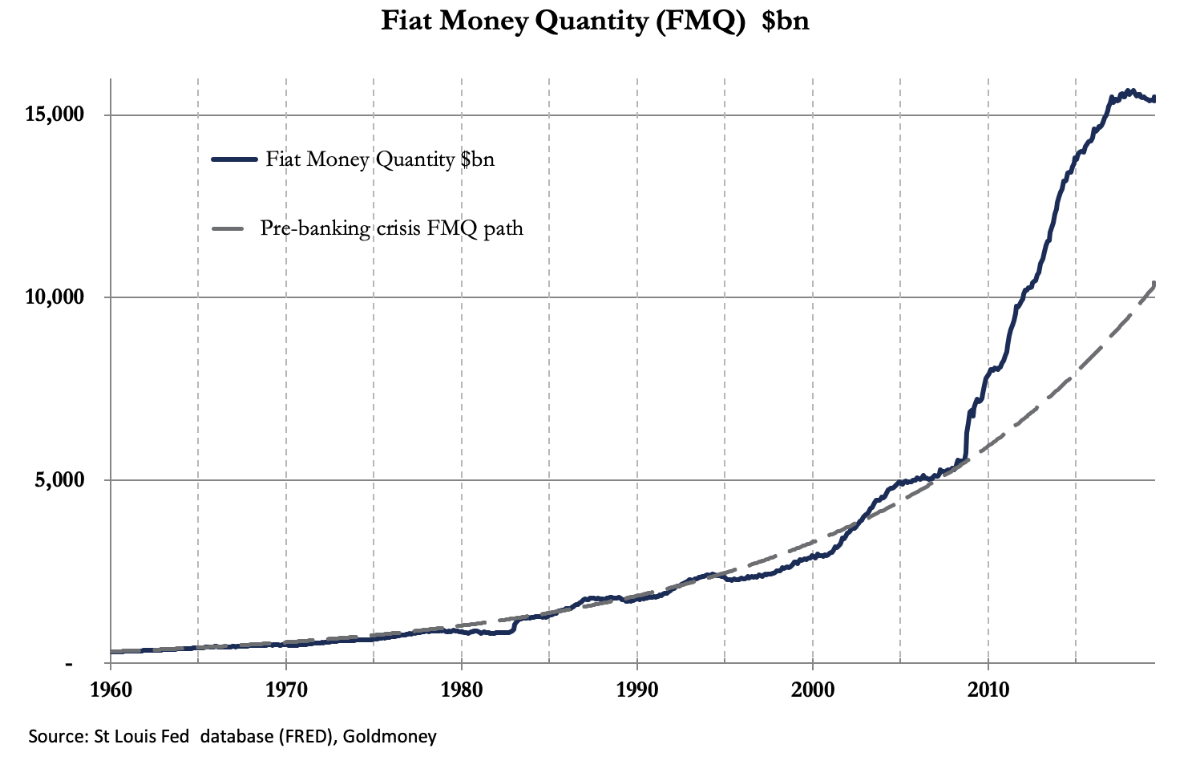

Listening to recent commentaries about the repo failures in New York leads one to suppose there is insufficient money in the system. This is not the real issue, as the chart below of the fiat money quantity for the dollar clearly shows.

The fiat money quantity is the amount of fiat money (in this case US dollars) both in circulation and held in reserve on the central bank’s balance sheet. Before the Lehman crisis, it grew at a fairly constant compound growth rate of 5.86%. Since the Lehman crisis, it has grown at an average of 9.45%, even after the slowdown in its rate of growth that started in January 2017. FMQ is still $5 trillion above where it would have been today if the massive monetary expansion in the wake of the Lehman crisis had not happened. If there is a shortage of money, it is because the process of debt creation to fund current expenditure is spiralling out of control.

It is not just the US. If we take similar (but less detailed) figures for FMQ in other major nations by adding together broad money M3 and central bank balance sheets, we find that it has increased at varying rates for the most important economies. In China, the compound annual growth rate has been 12%, though the growth in Japan at 5.2% and in the Eurozone at 4.9%. has been more subdued, reflecting stagnant levels of bank credit. When for the lack of any other measure statisticians use a GDP money total as a substitute for defining economic progress, we should not be surprised to see that the economies with the greatest rate of monetary growth are reckoned to be the best performing.

The Rest…HERE